How Thoma Bravo Grew Ellie Mae from $3.7B to $11B in 18 Months

How Thoma Bravo Grew Ellie Mae from $3.7B to $11B in 18 Months

Private Equity Case Study

Parties Involved

Ellie Mae

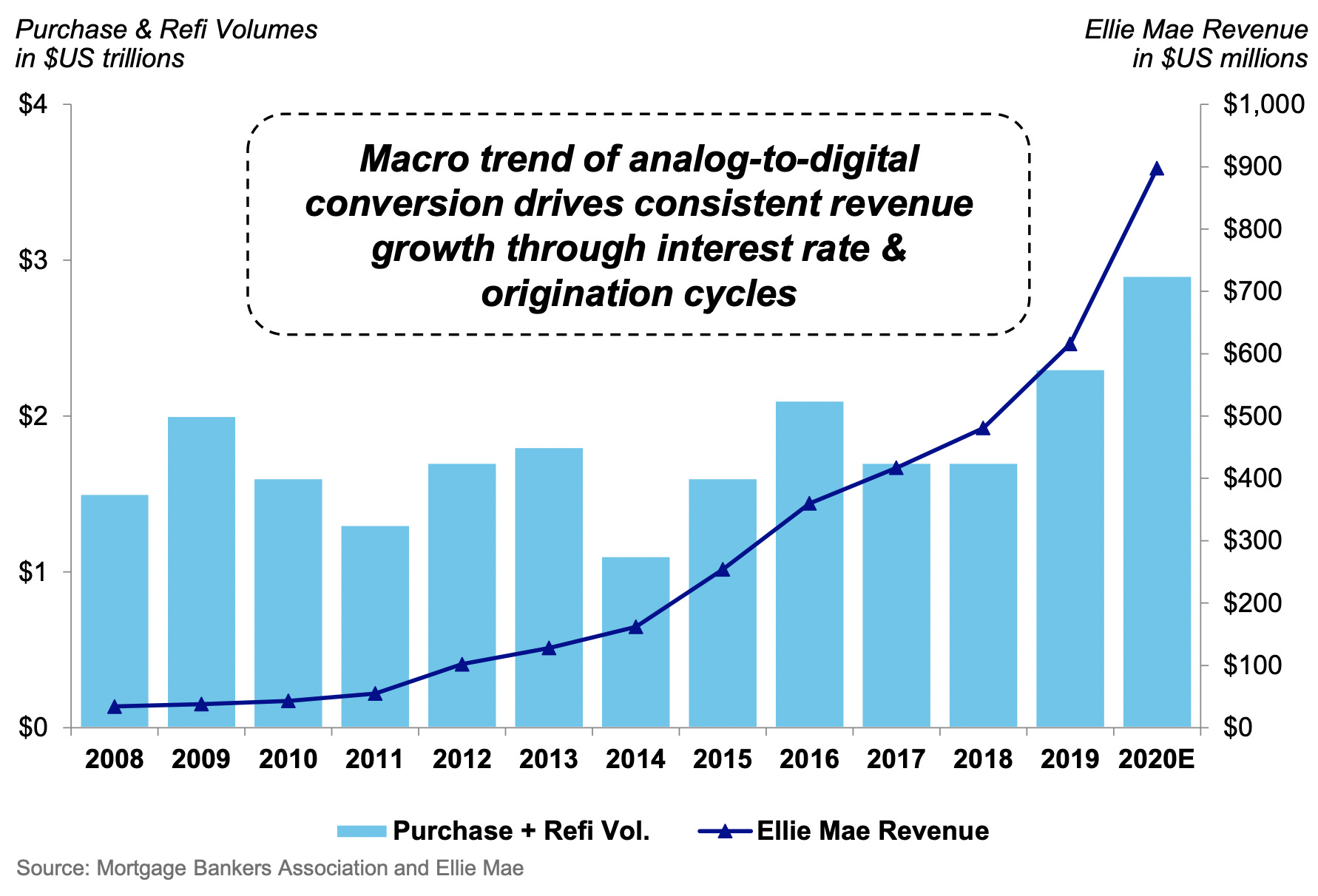

Ellie Mae, a pioneer in cloud-based technology solutions for the mortgage finance industry, soared to prominence after its IPO in April 2011 at $6 per share. However, the company faced challenges in 2018 as mortgage rates increased, causing a significant drop in its share price. By mid-2018, Ellie Mae's market value had plummeted from its peak, reaching an opportune moment for private equity involvement.

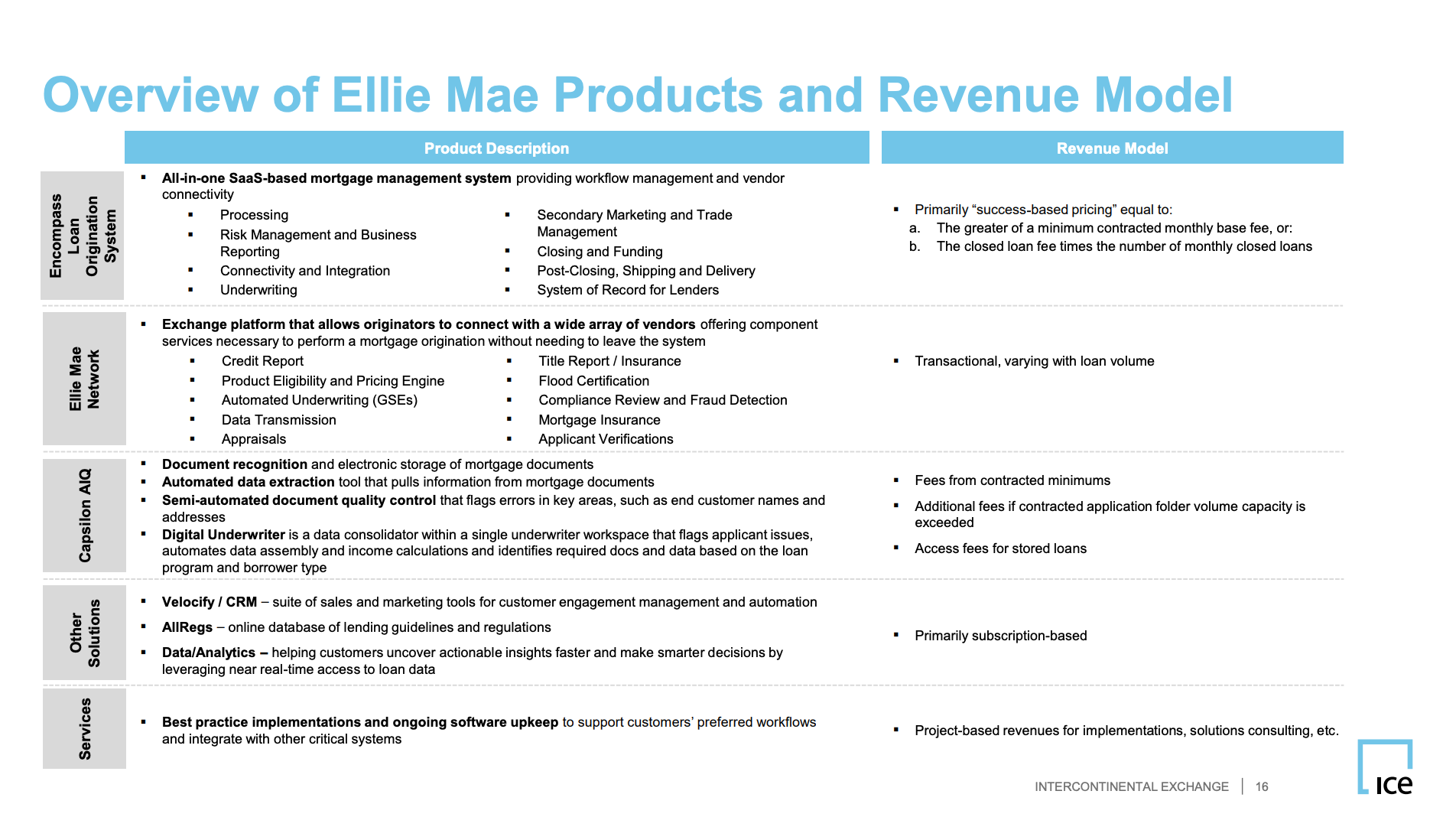

See appendix of a description of Ellie Mae’s product offerings and business model.

Thoma Bravo

Enter Thoma Bravo, a powerhouse in the private equity world, specializing in software and technology investments. One of the largest and most active software investors in the world, the firm recognized the untapped potential in Ellie Mae's downturn and seized the opportunity to purchase a diamond in the rough.

Intercontinental Exchange (ICE)

Intercontinental Exchange, a Fortune 500 company, played a pivotal role in the later stages of this narrative. As the parent company of the New York Stock Exchange, ICE would become the strategic acquirer of Ellie Mae.

The Price Drop

In April 2011, Elli Mae IPOed at $6 per share. From IPO to 2016 to mid-2018, shares rose to over $100. Ellie Mae was the type of stock that “buy-and-hold investors own in perpetuity,” according to Forbes [2]. However, when the Fed’s rate hikes led to an increase in mortgage rates in 2018, Ellie Mae’s processing revenue took a hit, causing investors to abandon the company. Between August and November 2018, Ellie Mae’s shares shed some 50% of their value as CEO Jonathan Corr cited “rising rates, low housing inventory, and overall home affordability” as significant headwinds to their business during their third quarter earnings report [3].

Thoma saw this as a strategic opening.

The Purchase

On February 11th, 2019, Ellie Mae's shares closed at $81.92, marking a turning point [4]. The next day, Thoma Bravo announced an all-cash acquisition of Ellie Mae at $99.00 per share, offering shareholders a 49% premium to the 60-day average closing price as of February 1st. Despite this premium however, Thoma was more than happy to make such an offer–$99 was still nearly 20% below Ellie’s midyear high [5]. The offer represented a $3.7 billion purchase price, with the buyout firm putting up about $2.2 billion of equity [6].

Thoma Bravo was off to the races.

Operational Excellence

Within 18 months, Thoma Bravo swiftly implemented operational changes to steer Ellie Mae back on course. The strategy included cost reduction, layoffs, stock-based compensation reduction, price increases, and a strategic add-on acquisition.

Reducing Cost

Though specifics haven’t been released publicly, Thoma Bravo’s Managing Partner Holden Spaht tells Buyouts that they streamlined Ellie’s cost structure and “redirect[ed] sales and product resources to the core business” [6]. Spaht talks about a restructuring around Ellie Mae’s go-to-market organization, which most likely meant a headcount reduction.

Layoffs

In May, Elli Mae underwent an official wave of layoffs, letting go over 10% of its workforce. Smaller batches of layoffs occurred later in the year and in early 2020 according to TheLayoff.com [7]. Thoma retained Ellie Mae’s existing management team, with employees speculating that most of the layoffs were in the sales and account management divisions.

Stock-based Compensation

Employee stock-based compensation saw a notable reduction following Thoma Bravo's involvement. After ICE's acquisition of Ellie Mae and the smaller, ~300 employee business, Bridge 2Solutions, employee headcount surged by 48% from 5,989 to 8,890. Surprisingly, during this growth, stock-based compensation decreased by 9%, dropping from $139 million to $127 million [8]. Ellie Mae's 2018 10-K reports a stock-based compensation expense of $40 million with 1,570 employees. This implies that stock-based compensation per head declined from $23.2K at ICE and $25.5K at Ellie Mae to $14.3K at the pro-forma company. The reduction signifies a substantial 38% decrease for ICE and an even more significant 44% decrease for Ellie Mae, showcasing Thoma Bravo's slash to stock-based compensation.

Price Increases

Ellie Mae’s pricing isn’t publicly available and is typically provided through personalized quotes via the company’s sales team. Though, Spaht talks about Ellie’s software being underpriced “relative to the value it was delivering” making us assume that subscription and transactions fees were increased across Ellie Mae’s suite. This would be in line with Thoma’s typical operational strategy, who has a history of increasing prices 2-3 times over, as was the case with recent portfolio company Adenza (another $10Bn+ sale) [9].

Add-on Acquisition

Finally, Thoma Bravo orchestrated the acquisition of purchase mortgage automation software provider Capsilon for $350 million from Francisco Partners. Capsilon is the leading provider of AI-powered mortgage automation software for mortgage lenders, investors and servicers. This add-on greatly increased Ellie’s TAM and expanded its product offerings through new machine learning and natural language processing technologies. Capsilon added about $20 million of EBITDA would allow Ellie’s customers to more accurately recognize and extract data from mortgage applications.

An Incredible Turnaround

As interest rates plummeted to record lows in 2020, mortgage rates followed suit, leading to a surge in purchase and refinancing volumes. For Ellie Mae, business was booming.

Altogether, Thoma Bravo's operational enhancements propelled Ellie Mae's organic growth from 6% to a staggering 50% [6]. EBITDA margins surged from an average of 29% in the last five years of being a public company to over 50% in 2020 [10].

The Exit

After talks with Thoma, on August 6, 2020, ICE entered a definitive agreement to acquire Ellie Mae for $11.4 billion. The acquisition consisted of $9.5 billion in cash and $1.9 billion of ICE stock. ICE saw this investment as an opportunity finally have a strong footing in mortgages and lean further into technology.

For Thoma Bravo, this marked a remarkable exit at a 4.1x MOIC and a gross IRR of an astounding 217%, according to Spaht. We analyze Thoma’s return on our own below.

Return Attribution Analysis

The analysis makes the assumption that 10% of the debt is paid down (32% of 2020 EBITDA) over the 18 months. The actual debt paydown figure has not been reported.

Thoma Bravo sold Ellie at a significantly greater revenue multiple but a substantially lower EBITDA multiple. If Ellie Mae had been valued on a revenue multiple, there was an even split between Thoma’s return coming from revenue growth and multiple expansion. However, if Ellie Mae had been valued on an EBITDA multiple, the return was all from EBITDA growth.

The sale of Ellie Mae was a signature deal for Thoma's then flagship fund, Fund XIII, nearly matching the size of the $12.6 billion fund.

Conclusion

Thoma Bravo's journey with Ellie Mae stands as a testament to the power of strategic private equity intervention.

If you enjoyed reading this case study, consider subscribing below. We will continue to profile many more stand-out private equity investments like this one.

Appendix

Ellie Mae’s product descriptions and revenue models:

Sources

[6] https://www.buyoutsinsider.com/deal-of-the-year-thoma-bravo-with-ellie-mae/

[7] https://www.thelayoff.com/ellie-mae

[8] https://d18rn0p25nwr6d.cloudfront.net/CIK-0001571949/5ef1e14d-8463-4790-b2cc-262000b178ae.pdf

[9] https://www.theinformation.com/articles/inside-thoma-bravos-software-playbook

[10] https://s2.q4cdn.com/154085107/files/doc_presentations/2020/ICE_Ellie-Mae_Transaction_vF2.pdf

I came here through reddit. This is a great breakdown, I have subscribed. I hope to see more of this in the future!

Hey! This was a great analysis, but I have one question for you: how did you calculate the IRR over an 18 month period?